The downfall of a hero or one of the most surreal headlines ever?

| July 10, 2008 |

Searching for the 'Golden Goose'?

For years we have been speaking and writing about the massive bind the Fed now finds itself in. With price inflation rising – read as food and energy skyrocketing -- and little hope for nominal interest rate increases – read as housing too weak for higher rates – negative real interest rates (nominal rates less inflation) looks set to persist for some time.

Now why is that important?

Firstly, not only do negative real interest rates make holding non-income producing assets such as gold attractive, but an environment where inflation is allowed to have its way and economic growth is sick (stagflation), is tantamount to the perfect storm for gold stocks and other precious metals!

So what do you do?

You load up on assets leveraged to the price of gold – namely gold stocks.

Wrong!

As old gold bulls, we have seen this situation before. A low growth high inflationary environment is poisonous for equities – gold stocks included. And whilst the storm persist in the equity markets it will either drag gold stocks lower or prevent them from fully expressing themselves to the upside! That’s why we encourage investors to have a portion of their portfolio exposed directly to the metal either through ETFs, futures or physical:

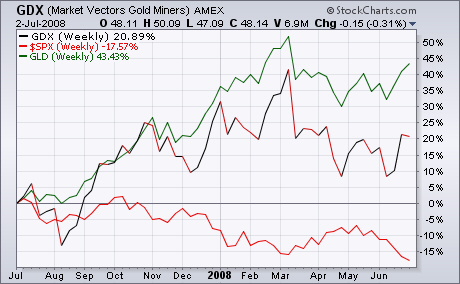

Chart 1 - Since July 2007 the S&P (red) has been moving lower and gold the metal (green) has outperformed gold equitites (red and black)

There is no doubt that an equity risk premium has weighed heavily on precious metal equities and that stabilization in equity markets would certainly benefit such stocks. But that’s old news.

What we consider interesting and downright fascinating is the nature of gold equities investors should be focusing on over the next year.

Conventional wisdom is that the juniors are where the investment gems lie. We don’t disagree – entirely.

Over the longer term (3-5 years) the fundamentals certainly favour late stage explorers and emerging producers, but an overlooked market dynamic causes us to lean rather towards their larger cousins.

As we have alluded to above, gold stocks and other precious metal equities are equities and more often than not subjected to the same forces as the general equity market. One such force is the veritable wall of passive indexed money, by some accounts amounting to several trillions of dollars.

And what’s the passive indexed money saying?

Chart 2 - large caps now outperforming small caps

Firstly, it’s saying that the long period of outperformance by small caps versus large caps (chart 2 is falling) bottomed in 2006 and the trend has since been towards large caps.

Secondly:

Chart 3 - large cap growth has outperformed value since late 2006

The trend in large caps from value to growth (chart 3 is falling) also looks to have bottomed around late 2006. We define growth as earnings growth of +15% p.a. and/or PEG ratio of around 1.5.

These trends resonated well with us as large cap gold producers beat out small cap miners over the last year leaving many a gold stock speculator highly frustrated.

Where to find such elephants that will benefit from these trends?

We would begin by looking at components of the Gold Stocks ETF (GDX) or the Amex Gold Bugs Index (HUI).

"The figures cited by both Martin and Pimentel include only a plant's production of ethanol, not the water it takes to grow corn. After adding that, about 1,700 gallons are needed to produce every gallon of ethanol, Pimentel said.

The entire water-use picture, coupled with the fuel it takes to produce ethanol, makes long-term, mass production of ethanol unsustainable, Pimentel said.

"I wish it were sustainable, I'm an agriculturalist," he said. "I wish this whole ethanol deal was a major benefit, but you've got to be a scientist first and an agriculturalist second."

Newsweek reported:

In the arid regions of the American West,water has always been a precious liquid gold. But in Adamson's home of Yuma County, Colorado, two hours east of Denver, the stakes just got higher. Thanks to the boom in ethanol production spurred by green-energy concerns, corn farmers in Yuma County—one of the top three corn-producing counties in the country—are enjoying a new prosperity.But the green-fuel boom touted as a clean, eco-friendly alternative to gasoline is proving to have its own dirty costs. Growing corn demands lots of water, and, in eastern Colorado, this means intensive irrigation from an already stressed water table, the great Ogallala Aquifer. One sign of trouble: in just the past two decades, farmers tapping into the local aquifers have helped to shorten the North Fork of the Republican River, which starts in Yuma County, by 10 miles. The ethanol boom will only hasten the drop further, say scientist and engineers studying the aquifers. The region's water shortage has pitted water-hungry farmers against one another. And lurking in the cornrows: lawsuits and interstate water squabbles could shut down eastern Colorado's estimated $500 million annual ethanol bonanza with the swing of a judge's gavel. Collectively, "[ethanol] is clearly not sustainable," says Jerald Schnoor, a professor of engineering at the University of Iowa and co-chairman of an October 2007 National Research Council study for Congress that was critical of ethanol. "Production will have serious impacts in water-stressed regions." And in eastern Colorado, there's lots of water stress.

Michael Grunwald reports that one person could be fed 365 days "on the corn needed to fill an ethanol-fueled SUV". He further reports that though "hyped as an eco-friendly fuel, ethanol increases global warming, destroys forests and inflates food prices." Environmentalists, livestock farmers, and opponents of subsidies say that increased ethanol production won't meet energy goals and may damage the environment, while at the same time causing worldwide food prices to soar. Some of the controversial subsidies in the past have included more than $10 billion to Archer Daniels Midland since 1980. Critics also speculate that as ethanol is more widely used, changing irrigation practices could greatly increase pressure on water resources. In October 2007, 28 environmental groups decried the Renewable Fuels Standard (RFS), a legislative effort intended to increase ethanol production, and said that the measure will "lead to substantial environmental damage and a system of biofuels production that will not benefit family farmers...will not promote sustainable agriculture and will not mitigate global climate change."To a large degree, this crisis is man-made — the result of misguided energy and farm policies. When President Bush and other heads of state of the Group of 8 leading industrial nations meet in Japan this week, they must accept their full share of responsibility and lay out clearly what they will do to address this crisis.

To start, they must live up to their 2005 commitment to vastly increase aid to the poorest countries. And they must push other wealthy countries, like those in the Middle East, to help too. That will not be enough. They must also commit to reduce, or even better, do away with their most egregious agricultural and energy subsidies, which contribute to the spread of hunger throughout the world.

In the last year, the price of corn has risen 70 percent; wheat 55 percent; rice 160 percent. The World Bank estimates that for a group of 41 poor countries the combined shock of rising prices of food, oil and other raw materials over the past 18 months will cost them between 3 and 10 percent of their annual economic output.

Some of the causes are out of governments’ control, including the rising cost of energy and fertilizer, and drought in food exporters like Australia. Higher consumption of animal protein in China and India has also driven demand for feed grains. Wrongheaded policies among rich and poor nations are also playing a big role.

Of those, perhaps the most wrongheaded are the tangle of subsidies, mandates and tariffs to encourage the production of biofuels from crops in the United States and the European Union. According to the World Bank, almost all of the growth in global corn production from 2004 to 2007 was devoted to American ethanol production — pushing up corn and animal feed prices and prompting farmers to switch from other crops to corn.

Long-standing farm subsidies in the rich world have also contributed to the crisis, ruining farmers in poor countries and depressing agricultural investment.

Rich countries are not the only culprits. At least 30 developing countries have imposed restrictions or bans on the export of foodstuffs. Importing countries are now stockpiling supplies, which takes more food from global markets. Export barriers also reduce farmers’ profits and discourage them from investing in more production.

So far there is no sign that the leaders of the developed countries are ready to do what is needed. The United States and Europe have refused to curtail their bio-fuel subsidies or their lavish farm subsidies. They are also falling far short of their aid commitments.

At the 2005 G8 summit meeting, leaders said that by 2010 wealthier nations would increase annual development aid to poor countries by $50 billion. Yet aid has increased by only $11 billion. And there is suspicion that the G8 nations, who were to provide the lion’s share of the increase, want to wiggle out of their commitment.

We welcome President Bush’s pledge to provide $5 billion this year and next to “fight global hunger,” but much more must be done. The United States remains the stingiest of rich nations when it come to foreign aid.

In a letter to heads of state of the G8, Robert Zoellick, the World Bank president, estimated that the bank needs $3.5 billion to provide immediate food aid and seed and fertilizer in poor countries. The International Monetary Fund and the World Food Program estimate they need $6.5 billion more in the short term to help feed vulnerable populations. This does not even count the need for essential longer-term investments to increase farm productivity in poor nations in Africa and elsewhere.

As Mr. Zoellick wrote, the food crisis is a test of the world’s willingness to help the most vulnerable. The leaders gathered in Japan must rise to the challenge.

The European Central Bank, as expected, raised interest rates a quarter point to 4.25% in a bid to attack inflation despite signs of weakening growth. The U.S. Federal Reserve, meanwhile, appears to be on hold for the coming months — despite rising inflation concerns — to give the economy more time to recover from the turmoil in housing, credit, labor and energy markets. Their divergence might be explained by the central banks’ mandates: the ECB is charged with maintaining price stability first, while the Fed aims to achieve low inflation and optimal growth at the same time.

But the difference in mandates or even economic circumstances between the U.S. and Europe don’t quite account for the divide, Deutsche Bank economists say in a research note this week titled “ECB is from Mars and Fed is from Venus.” As chief economist Peter Hooper explains, “The two central banks are reacting to relatively similar economic and financial circumstances as if they are from different planets, with the ECB’s approach akin to a frontal attack on inflation that the Roman god Mars would have approved of, while the Fed is being more cautious and patient, in a manner the goddess Venus would have endorsed.”

The Deutsche Bank economists say the divergence comes from the two regions’ different historical experiences in dealing with the shock from deflating asset prices and rising inflation.

In the United States: “The traumatic experience of the deflation and extreme levels of unemployment that occurred during the Great Depression in the 1930s – and the Fed’s mistakes during this period — play a prominent role in the discussion of monetary policy by both practitioners and academics. Accordingly, Fed policy makers have been very sensitive to the risk of asset price collapses and debt deflation (note, for example, the Fed’s reaction to the 1987 stock market crash, the [Long-Term Capital Management] crisis, and the burst of the dot-com bubble).”

In Europe: “Probably the most prominent economic trauma in Europe were Germany’s hyperinflation after World War I and currency reform after World War II. Throughout its existence the Bundesbank was extremely sensitive to inflation pressures, and willing to take significant risks with growth to keep inflation in check (note, for example, the Bundesbank’s reaction to the two oil shocks of the 1970s and its reluctance to follow the Fed in 1987). German sensitivity to inflation risks of course had a strong influence on the institutional design of the ECB and more recently on the implementation of the euro zone’s monetary policy.”

Of course, Fed officials in recent weeks have ratcheted up their talk about “vigilance” of inflation and inflation expectations. But most policy makers appear inclined to wait as long as they can to give their rate cuts of the last year a chance to work. And the ECB won’t necessarily be following today’s rate increase with more tightening. The Deutsche Bank economists say the the transatlantic policy divergence will diminish when weaker growth in Europe lowers fears at the ECB and even leads to rate cuts in 2009, while the Fed remains on hold. “What now looks like the beginning of a new transatlantic divergence of monetary policy,” they write, “will in our view eventually look like a blip in the time-tested relationship of the Fed leading and European central banks following.” - Sudeep Reddy

| Economic Growth and Employment | |

|---|---|

|  |

|  |

| Consumer Activity | |

|  |

| |

| Inflation | |

|  |

| Housing Construction and Sales | |

|  |

| International Trade | |

| |